Fishing in a Bigger Pond

Many Australian investors have a home-market bias whereby their portfolios have a large allocation to Australian shares, due to familiarity with companies or a bias to favourable tax treatment of fully franked dividends (i.e. no double taxation of dividends). The Australian share market is an attractive market to generate income and capital gains with a relatively high degree of cyclicality, given the large banking and mining sector exposure.

Many Australian investors have a home-market bias whereby their portfolios have a large allocation to Australian shares, due to familiarity with companies or a bias to favourable tax treatment of fully franked dividends (i.e. no double taxation of dividends). The Australian share market is an attractive market to generate income and capital gains with a relatively high degree of cyclicality, given the large banking and mining sector exposure.

For investors with a focus on long term capital gains we contend that international share markets should be a core pillar of portfolio allocations. This is underpinned by several facts: (1) the Australian share market is a very small global investment universe, (2) a larger opportunity set provides a more fertile hunting ground, and (3) international companies generate higher returns on capital and reinvest those returns more than Australian companies.

In this article we look at two sectors where we have high conviction and within these sectors compare Australian listed companies with their international peers. This demonstrates the superior quality and risk-reward characteristics on offer for investors with the scope to look outside their own investment backyard.

Information Technology: Oligopolies and Monopolies

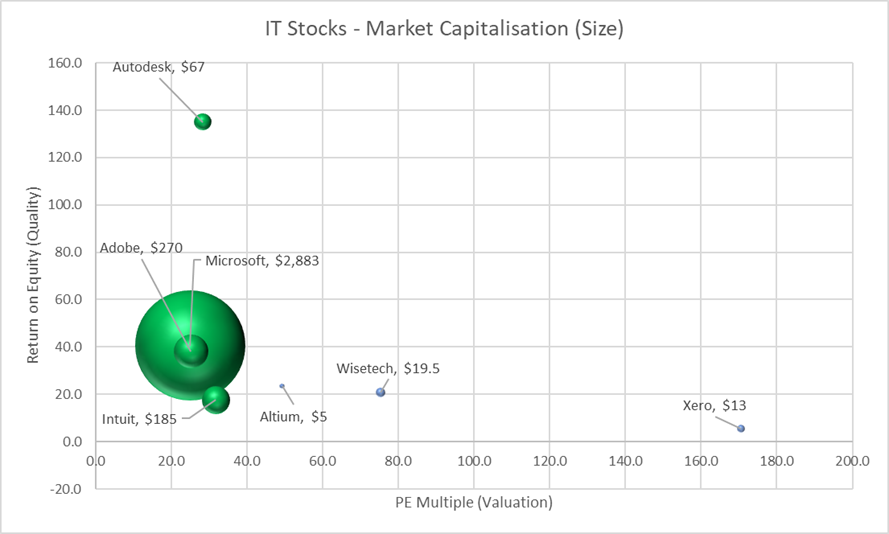

The sector that best illustrates the significant disparity between Australian listed companies and offshore counterparts is Information Technology, where network effects and scalable business models result in winner take all dynamics. This has meant that global leaders such as Microsoft and Adobe have continued to grow at a high cadence over many years despite their enormous size. This growth has not come at the detriment of quality, with these companies delivering strong returns on equity, nor has it resulted in lofty valuation multiples. In comparison, the Australian share market is a much smaller opportunity set, which tends to result in higher growth stocks trading on higher valuations when compared to their global peers. As a result, we think that the risk-reward is skewed in favour of international IT stocks when compared against their Australian peers.

Above: US listed (green) technology companies dwarf ASX listed (blue) technology stocks, both in terms of sheer size (10x to 100x market capitalisation) as well as quality (higher return on equity) and valuation (lower Price-Earnings multiples). For example, Adobe trades on a PE ratio of 25 and generates a Return on Equity of 40%.

Health care: Australian companies punch above their weight, but there are complimentary exposures offshore

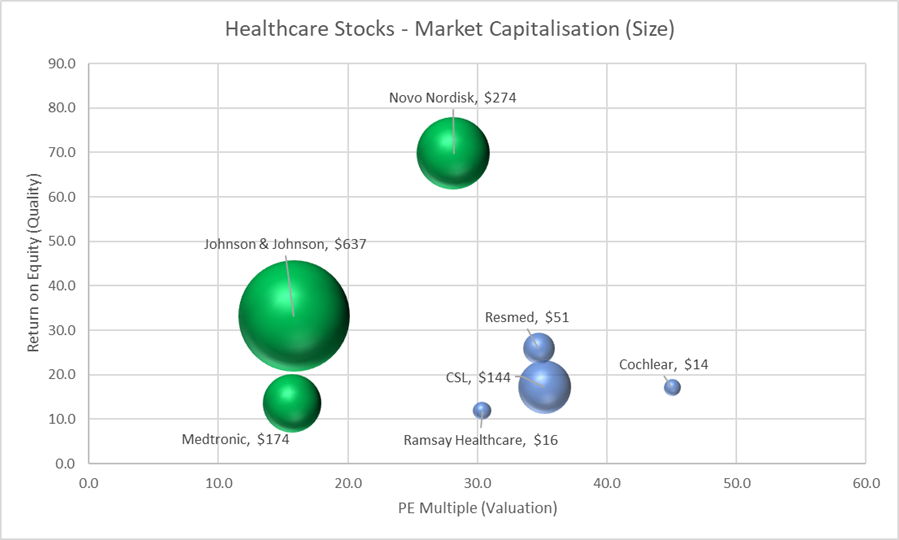

The Australian healthcare sector punches well above its weight in a global context, as we have several high-quality companies that developed products to treat previously unmet conditions, and in the process wide economic moats and significant shareholder returns. These include Commonwealth Serum Laboratories (CSL), Cochlear (Bionic Ear) and ResMed (Obstructive Sleep Apnea). That said, we think it is worthwhile taking a global approach to put these Australian success stories into context and consider a few alternatives in a well-diversified portfolio.

There are several points we want to make when discussing Australia’s largest healthcare company, CSL. Firstly, it is one of the highest quality companies on the ASX and secondly it trades on a premium valuation multiple that reflects that quality – CSL trades at double the valuation of the broader market. A key reason for the valuation premium is the home-market bias of Australian investors and limited opportunity set here on the ASX.

We have discussed CSL’s inherent quality characteristics with clients over many years, which ultimately stem from a long lasting and successful research and development program that has delivered a portfolio of biopharmaceutical products that treats haemophilia, immune deficiencies, and influenza. To quantify CSL’s quality we refer readers to its return on equity of 17%, earnings growth of 17% per annum and share price growth of 20% per annum over the last 20 years. This is one of the strongest long term track records of a major company in the Australian share market.

Another global healthcare company that we draw readers attention to is Novo Nordisk, a Danish listed company that is double the size of CSL, that owns a portfolio of products to treat diabetes and related illnesses. Over the last 20 years Novo has the same earnings and share price growth as CSL, which is just one example of a global leading healthcare business that is a potentially complementary investment exposure for CSL holders.

Our View

In closing, we advocate investing in a globally diversified portfolio of high-quality investments that is relatively agnostic about where companies are geographically domiciled. This approach means that we have a large opportunity set from which to draw upon and means that we can objectively compare Australia’s best against the best in the world. Healthcare is one sector where we hold Australian companies in high regard, investing in global leaders such as CSL, ResMed and Ramsay Healthcare. We have a high conviction view that investors should seek out international leaders in sectors such as Information Technology, where there is a significant premium in quality, growth and valuation characteristics versus Australian counterparts.

Investors that are interested in expanding their international investment opportunities should speak with their adviser.

Disclaimer: This publication has been compiled by Financial Decisions (AFSL/ACL Number 341678). Past performance is not a reliable indicator of future performance. While every effort has been taken to ensure that the assumptions on which the outlooks given in this publication are based on reasonable data, the outlooks may be based on incorrect assumptions or may not take into account known or unknown risk and uncertainties. Material contained in this publication is an overview or summary only and it should not be considered a comprehensive statement on any matter nor relied upon as such. The information and any advice in this publication do not take into account your personal objectives, financial situation or needs. Therefore you should consider its appropriateness having regard to these factors before acting on it. While the information contained in this publication is based on information obtained from sources believed to be reliable, it has not been independently verified. To the maximum extent permitted by law: (a) no guarantee, representation or warranty is given that any information or advice in this publication is complete, accurate, up-to-date or fit for any purpose; and (b) Financial Decisions nor its employees are in any way liable to you (including for negligence) in respect of any reliance upon such information or advice. December 2022

Contact: Financial Decisions PO Box 484 Mona Vale NSW 1660, T 02 9997 4647, F 02 9997 7407