Expect the Unexpected

Investing is an uncertain past-time. After a fairly smooth 2017, the past twelve months have shown equity investors what “Mr Market” is capable of when he wakes up. To summarise, we experienced the volatility entrée in February and March 2018, followed by the calm before the storm between May and September. To end the year, we saw a trifecta of negative news that brought the markets down by 20% in a single quarter with December giving investors the biggest scare.

Then came the turnaround. US Federal Reserve Chairman, Jerome Powell, indicated in early January 2019 that they would be patient and pause the interest rate hikes they were focused on doing for the past 18 months. The market rejoiced and since then investors have gone back to the races, pushing most markets back to where they were pre the December quarter.

The above summary shows how quickly markets can ebb and flow and how foolish investors would be if we were to react to such news by selling at the lows and buying back at the highs. Welcome to the uncertain world of investing. As we often hear in investing – the only certainty is that markets will remain uncertain.

Our current view and positioning

To provide our clients with a framework of how we view the current market, we see several things that investors must come to terms with when investing –

- The end of Quantitative Easing (QE) is now met by the uncertainty of Quantitative Tightening by the US (essentially this is the withdrawal of money from the financial markets)

- Valuation levels are at fair value or above (meaning that good opportunities in equities and bonds in general are no longer easy to find)

- Future of interest rates

- Politics and policy decisions could affect the shorter-term price actions of assets

- A likely slowdown of economic activity domestically and worldwide after a two-year period when the financial markets were “firing on all cylinders”

In our domestic market, we need to prepare for the following –

- Labor’s proposed policy changes on such items as franking credits and Capital Gains tax (refer to our previous Views newsletter) if they were elected into Government

- A possible continuation of the deflation in overall house prices

- The Reserve Bank indicating that a rate cut could be in the works this year

- Changes proposed from the Royal Commission that is likely to affect the financial services sector and unemployment over the medium term

With the above as reference points, we would consider the strong returns like those experienced between late 2016 to early 2018 are unlikely to be matched over the next two-year period.

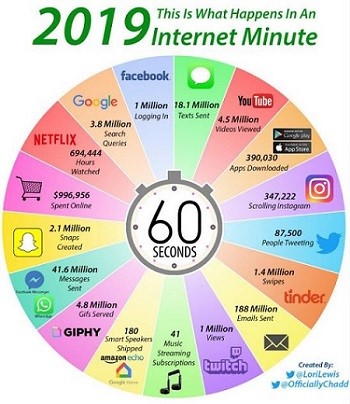

On top of that, investors must all learn to grapple with technological changes and the fast-changing world we are living in. The wheel graph below was taken from Cuffelinks, showing the amount we buy online per minute, what we view, who we talk to, what we share and literally who we are as a person, when we sign up to any of these online platforms.

With these less than glowing scenarios painted, there is always a silver lining – good prices never come with good news. When uncertainty (typically measured by the volatility index – VIX) reaches an apex, investors are greeted with far better prices. In general, we are taking a more cautious stance than at any time over the last two years. Changes have mainly come from a slight reduction in weightings in the equity sector and increasing a little on the fixed income sector to enable some capital protection if we were to experience another correction this year. However, these changes are more about the headwinds we pointed out above and the market cycle we are in right now and not about the fundamental strengths of the investments we have allocated your money in.

Clients who have been with us for many years know that you will always come out fine if you stick to your game plan and not buckle under the pressure of an always uncertain market.

If you are having problems making sense of it all, please feel free to contact your adviser to review your financial health.

Disclaimer: This publication has been compiled by Financial Decisions (AFSL/ACL Number 341678). Past performance is not a reliable indicator of future performance. While every effort has been taken to ensure that the assumptions on which the outlooks given in this publication are based on reasonable data, the outlooks may be based on incorrect assumptions or may not take into account known or unknown risk and uncertainties. Material contained in this publication is an overview or summary only and it should not be considered a comprehensive statement on any matter nor relied upon as such. The information and any advice in this publication do not take into account your personal objectives, financial situation or needs. Therefore you should consider its appropriateness having regard to these factors before acting on it. While the information contained in this publication is based on information obtained from sources believed to be reliable, it has not been independently verified. To the maximum extent permitted by law: (a) no guarantee, representation or warranty is given that any information or advice in this publication is complete, accurate, up-to-date or fit for any purpose; and (b) Financial Decisions nor its employees are in any way liable to you (including for negligence) in respect of any reliance upon such information or advice. April 2019

Contact: Financial Decisions PO Box 484 Mona Vale NSW 1660, T 02 9997 4647, F 02 9997 7407