Welcome to the June edition of our Exchange Newsletter.

In this edition, we look at the importance of getting the right advice when it comes to assessing the aged care options for you or your loved ones. As well as exploring the costs associated with moving into a retirement village or residential aged care, we also look at Home Care Packages (HCPs) that enable many people to access affordable care services while remaining in their home.

This edition also features information about the Federal Government’s announcement to extend minimum pension drawdown amounts, the establishment of Director Identification Numbers, plus carry-forward unused concessional super contributions.

But first, we’d like to introduce our new Chief Investment Officer, Daniel Rolley.

Introducing Daniel Rolley

Daniel Rolley

We are delighted to formally introduce you to Daniel Rolley, our new Chief Investment Officer.

Daniel has more than 18 years’ experience in investment markets, as both an Analyst and Portfolio Manager. Prior to joining Financial Decisions Daniel held roles with a range of institutions including Citigroup, Thomson Reuters and Eight Investment Partners, and most recently as Head of Research for a boutique investment advisory firm.

As Chief Investment Officer, Daniels’ responsibilities include directing the Investment Committee, managing the Investment team, overseeing portfolio construction and conducting investment analysis.

Daniel has a comprehensive range of specialist skills including Portfolio and Risk Management, Equities and Economic Research, Company Valuation and Modelling, and Investment Systems.

Daniel holds undergraduate degrees from the University of Sydney, in Commerce (Finance) and Engineering (Software) (First Class Honours) and is a CFA charter holder.

Aged care – have you got a plan?

Many of us don’t think about aged care services until we need to make a quick decision for either ourselves or on behalf of a family member. For instance, a parent may have a fall and health professionals deem them unfit to return home to look after themselves, or dementia may come on suddenly for a loved one. Often, we don’t have much time to think, plan or weigh up the options.

When faced with this situation, who makes the decision? Can you and your family afford your preferred model of aged care? What does it cost? What government assistance is available? Where do you start?

That’s why it’s so important to get the right advice about your aged care options before you’re forced into making crucial decisions in times of high stress.

Compared to most other countries, Australia is good at looking after our elderly, providing a range of options for dignified aged care living. The trick is to know what options are available to you and how to select the one that best suits you or your family member’s needs.

The value of an aged care adviser

The first step is to look at the government resource My Aged Care, which provides an overview of how the aged care system works. Then it’s time to speak to an aged care adviser. An aged care adviser helps take the emotion out of the decision-making process, as they have a clear understanding of the aged care options, what they cost, the help available to you, and what impact it has on your or your family’s finances.

What level of care is required?

You should also obtain an Aged Care Assessment Team (ACAT) assessment, which helps determine the level of care you or your family member requires and the options available, including:

- At home assistance

- Over 50s lifestyle or retirement villages

- Residential aged care with 24/7 medical support

How much does it cost?

Australia operates a means-tested approach to aged care, which means your assets and financial position influence the government subsidies you’re eligible for and the level of fees you’ll be required to pay. This can be a confusing and complicated process for families, which is why an aged care adviser can help explain the options and associated fees based on your financial position.

What’s more, your adviser can handle everything for you, including negotiating and liaising with the aged care facilities and government agencies such as Centrelink – saving you precious time and energy. They can also work with your accountant, financial adviser or family lawyer to ensure there are no surprises e.g. if one partner passes away, the surviving partner may lose access to government subsidies.

When entering an aged care facility, there are generally four types of fees you need to pay:

- A lump sum accommodation deposit – anywhere between $350,000 – $750,000.

- A basic daily fee, which is a percentage of pension that’s deducted to cover daily care.

- Means-tested care with annual and lifetime caps.

- Additional service fees– these are the ‘luxuries’ or added extras such as activities or hairdressing. Your aged care adviser can negotiate these fees on you or your family’s behalf.

At home assistance

For those who decide that staying in the home is the best option for themselves or their family member, a Home Care Package (HCP) can provide affordable access to in-home care services. Provided by a range of organisations across Australia, an HCP is designed for people whose care needs go beyond what the Commonwealth Home Support Programme provides e.g. you need help with everyday tasks or you require more complex or intensive care.

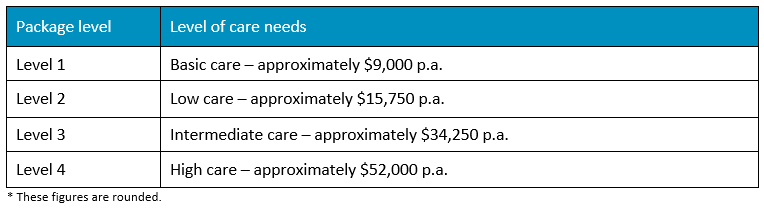

As everyone’s care needs are different, there are four HCP funding levels, including:

You’re expected to contribute to the cost of your care if you can afford it. Your contribution is made up of three types of fees:

- Basic daily fee (up to $10.85 from 20 March 2021) – Your provider may ask you to pay a basic daily fee based on your HCP level.

- Income-tested care fee (up to $31.14 from 20 March 2021) – Some people may also have to pay an income-tested care fee. Whether you pay it, and how much of it you pay, is determined by a formal income assessment via Services Australia. If you need to pay this fee, there are annual and lifetime limits on how much you can be asked to pay.

- Additional fees – Any other amount you have agreed to pay for extra care and services that wouldn’t otherwise be covered by your HCP. You can read more about the fees, caps and how to use your package funds here: Home Care Package costs and fees.

For more information about aged care options for either yourself or a loved one, please contact us on 02-9997 4647.

Reduced minimum pension drawdowns extended

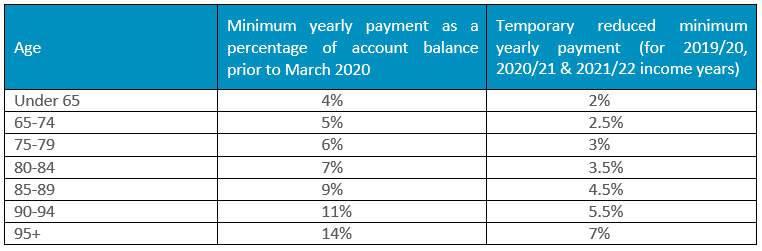

In an ongoing effort to minimise the financial impact of COVID-19 on older Australians, the Federal Government recently announced that the temporary reduced minimum pension drawdown amounts have been extended until 30 June 2022.

Introduced in March 2020 and originally due to return to standard levels on 1 July 2021, the reduced minimum amounts enable pension members to withdraw less of their retirement savings and keep a greater amount invested.

The standard and temporary rates for each age group are outlined in the table below:

If you have any questions or concerns about how these temporary minimum pension drawdown amounts may impact you, please contact us on 02-9997 4647.

Did you know you can top up your super with carry-forward unused concessional contributions?

From 2019/20, carry-forward rules allow you to make extra concessional super contributions over and above the general concessional contributions cap without having to pay extra tax. For many people, this is a prudent, tax effective way to top up their super balances.

The carry-forward arrangements involve accessing unused concessional cap amounts from previous years. An unused cap amount occurs when the concessional contributions you made in a financial year were less than your general concessional contributions cap.

To apply your unused cap amounts you need to meet two conditions:

- Your total super balance at 30 June of the previous financial year is less than $500,000; and

- You made concessional contributions in the financial year that exceeded your general concessional contributions cap.

The amount of unused cap amounts you can carry-forward depends on the amount you contributed in previous years, starting from 2018/19. You can use caps from up to five previous financial years.

The oldest available unused cap amounts are used first. For example, unused cap amounts from 2018/19 would be applied to increase your cap first, before unused cap amounts from 2019/20.

Unused cap amounts are available for a maximum of five years and will expire after this time. That means a 2018/19 unused cap amount which is not used by the end of 2023/24 will expire.

If, after applying all your available unused cap amounts, you still have excess concessional contributions, you may need to pay extra tax.

Director Identification Number

As part of its 2020 Budget Digital Business Plan, the Federal Government announced the implementation of the Modernising Business Registers (MBR) program.

The MBR program aims to make it easier for businesses to meet their obligations, enhance the accuracy of business information, allow businesses to spend more time on customers and business operations, and improve the efficiency of registry service transactions.

The MBR program also includes the introduction of a Director Identification Number (Director ID), which is a unique identifier that a director will keep forever. The Director ID will help:

- Prevent the use of false director identities

- Government regulators trace a director’s relationship with past companies

- Identify and eliminate director involvement in unlawful activity

Who needs a Director ID?

Eligible officers of a company or other body corporate registered under the Corporations Act 2001 (e.g. a corporate trustee of an SMSF or Trust) will need a Director ID. An eligible officer is a person who is appointed as a director or an alternate director acting in that capacity.

When should I apply?

You don’t need to do anything at this stage. The ATO is currently testing the new application process to ensure a seamless user experience and will provide an update in the coming months.

More information can be found on the ATO website: https://www.ato.gov.au/General/Gen/Modernising-Business-Registers/

Our condolences

Finally, we would like to offer our heartfelt condolences to Michael Phillips after the sad passing of his wife, Pip. Prior to the merge with Financial Decisions, Pip was a much-loved part of the Phillips Financial ‘family’. She was known to many of our clients, was Michael’s confidante and soul mate, and will be dearly missed by us all.

Disclaimer: This publication has been compiled by Financial Decisions (AFSL/ACL Number 341678). Past performance is not a reliable indicator of future performance. While every effort has been taken to ensure that the assumptions on which the outlooks given in this publication are based on reasonable data, the outlooks may be based on incorrect assumptions or may not take into account known or unknown risk and uncertainties. Material contained in this publication is an overview or summary only and it should not be considered a comprehensive statement on any matter nor relied upon as such. The information and any advice in this publication do not take into account your personal objectives, financial situation or needs. Therefore you should consider its appropriateness having regard to these factors before acting on it. While the information contained in this publication is based on information obtained from sources believed to be reliable, it has not been independently verified. To the maximum extent permitted by law: (a) no guarantee, representation or warranty is given that any information or advice in this publication is complete, accurate, up-to-date or fit for any purpose; and (b) Financial Decisions nor its employees are in any way liable to you (including for negligence) in respect of any reliance upon such information or advice. June 2021

Contact: Financial Decisions PO Box 484 Mona Vale NSW 1660, T 02 9997 4647, F 02 9997 7407