The Healthcare Sector

Investing in high quality and defensive companies benefitting from ageing populations

One of our favourite long term investment trends is found in the healthcare sector, which is a beneficiary of increased demand from ageing populations in developed markets and rising middle class in emerging markets. For example, in developed markets such as Australia, the over 65 population is expected to increase by 4% per annum, against a broader population growth of closer to 2%. These trends mean that expenditure on healthcare products and services will continue to rise over the coming decades, providing a favourable backdrop for high quality healthcare companies.

The listed healthcare sector is made up of several sub-segments, varying in risk and return characteristics. This spans early-stage biotechnology companies, through to mature pharmaceutical and medical devices businesses, diagnostics, and hospital providers, and ultimately the owners of the real estate assets. Most of the world’s leading healthcare businesses are located in offshore markets, however Australian healthcare companies such as Resmed, Cochlear and CSL are all dominant players in their respective niches. Our biggest reservation within Australian healthcare companies is that they typically trade at relatively high valuation multiples due to scarcity and home market bias, which means the prospective investment returns are not as attractive when compared to the larger universe of international listed healthcare companies.

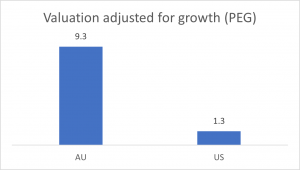

The Australian healthcare sector is nearly seven times as expensive as offshore healthcare companies, when adjusting for very expensive valuations and lower earnings growth vis-à-vis offshore companies. The chart below shows the Price-Earnings Growth ratio for the Australian and US listed healthcare sector, which is a valuation ratio adjusted for earnings growth. A rule of thumb is that a PEG ratio of around 1 to 2 represents good value for growth stocks. The Australian healthcare sector is significantly above this, indicating a generally expensive valuation.

Source: Financial Decisions

Our View

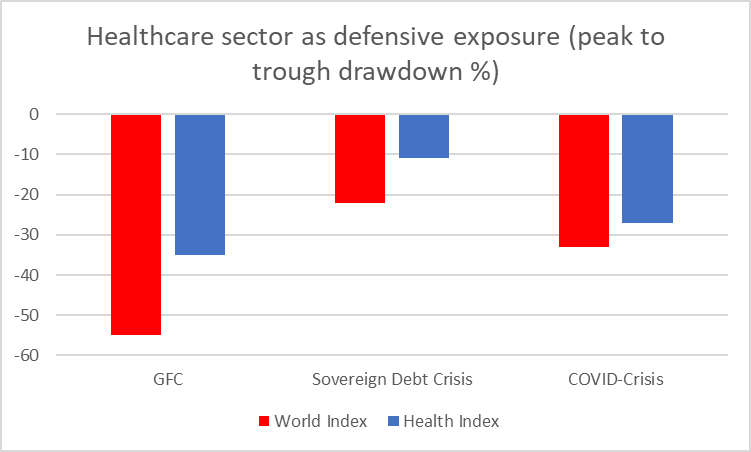

We think the healthcare sector has favourable investment characteristics, which stem from relatively high barriers to entry and generates a source of competitive advantage for those well capitalised healthcare businesses. These characteristics include generating above average returns on capital, above average earnings growth, and consequently sustainable capital (share price) growth. In addition to these above average returns, the healthcare sector is also relatively defensive during broad market selloffs, declining by less than the market. For example, during the GFC, the healthcare sector had a peak decline of 35% versus the broader market which declined by 55%, and more recently during the Covid-19 market drawdown, the sector declined by 27% versus the broader market of 35%.

The healthcare sector has defensive characteristics relative to the broader equity market, which include incurring smaller drawdowns during periods of market crisis. The chart below demonstrates this during several of these crisis periods, which saw the global healthcare sector fall by less than the market.

Source: Evans and Partners

Our Preferred Healthcare Investments

Our investment philosophy is to invest in leading companies that generate above average returns on capital and with strong financial position. Within the healthcare sector there are a range of businesses that meet these criteria that are listed both domestically and internationally. These include some of the largest healthcare businesses on the planet such as Johnson & Johnson, which is a diversified exposure across geography and business line, covering pharmaceuticals, medical devices and consumer products. We are also invested in the world’s largest pure-play medical device business, Medtronic, which provides products to address cardiac, neurological and spinal conditions and diabetes. Some of our favourite Australian listed healthcare businesses include biopharmaceutical leader CSL, hospital operator Ramsay and pathology provider Sonic Healthcare.

Clients should speak with their adviser to discuss whether some of the best healthcare companies in the world are suitable investments for their portfolio.

Disclaimer: This publication has been compiled by Financial Decisions (AFSL/ACL Number 341678). Past performance is not a reliable indicator of future performance. While every effort has been taken to ensure that the assumptions on which the outlooks given in this publication are based on reasonable data, the outlooks may be based on incorrect assumptions or may not take into account known or unknown risk and uncertainties. Material contained in this publication is an overview or summary only and it should not be considered a comprehensive statement on any matter nor relied upon as such. The information and any advice in this publication do not take into account your personal objectives, financial situation or needs. Therefore you should consider its appropriateness having regard to these factors before acting on it. While the information contained in this publication is based on information obtained from sources believed to be reliable, it has not been independently verified. To the maximum extent permitted by law: (a) no guarantee, representation or warranty is given that any information or advice in this publication is complete, accurate, up-to-date or fit for any purpose; and (b) Financial Decisions nor its employees are in any way liable to you (including for negligence) in respect of any reliance upon such information or advice. October 2021

Contact: Financial Decisions PO Box 484 Mona Vale NSW 1660, T 02 9997 4647, F 02 9997 7407