A Year of Transition and Opportunity

As 2025 draws to a close, three RBA rate cuts have eased pressure on borrowers, equity markets have continued their run and property prices have grown steadily in most capitals. It’s also been a year of change for Financial Decisions, with a new partnership setting us up for the future.

In our final Exchange for the year, our business leaders share their insights on the opportunities and challenges ahead for 2026.

Damien Cooper (outgoing CEO)

Behind the scenes, we’ve been working on something significant. Financial Decisions has joined forces with AZ NGA, a national advice platform that shares our approach to client relationships.

After 40 years as an independent practice, this was not a decision we took lightly. We reviewed the market options, and the partners and shareholders agreed that AZ NGA was the right fit for both the model and culture.

The partnership provides succession and growth solutions while we continue to operate independently as Financial Decisions, with the same team and philosophy. Our multidisciplinary model, with financial planning, accounting and wealth management under one roof, remains unchanged.

As part of this transition, I’m stepping back from the CEO role to focus on what I enjoy most: working directly with my clients as a Senior Adviser. Blake Conde, who has been leading operations for over a year now, steps into the CEO role. It’s a transition we’ve planned carefully, and I’m confident in where we’re headed.

You’ll hear from Blake below, along with insights from Daniel, Tim, Wade and Peter on what 2026 may hold across investments, lending and tax.

For more details on our partnership with AZ NGA, read the full announcement.

Blake Conde (Chief Executive Officer)

Taking on the CEO role at Financial Decisions is a privilege. I’ve spent the past year or two working closely with Damien and the leadership team on a gradual transition from Managing Director to CEO.

The reality is that running an advice business has become increasingly complex. Compliance, red tape and rising costs make it critical for practices to find efficiencies and stay focused on meeting evolving client needs. Our partnership with AZ NGA gives us access to resources and scale to deliver excellent service and advice.

For you, the day-to-day experience remains the same. Same advisers, same approach and same commitment to the families we work with across generations. The partnership supports what we’re already doing by enabling back-office efficiencies and access to best practices across a network of complementary firms.

Financial advice has always been about more than numbers for me. Having seen early in my career how unexpected events impact financial security, I’ve focused on helping families build solid foundations and long-term security. That multigenerational focus – from first-home buyers through to estate planning – is central to how we operate, and it’s not changing.

What excites me about this next chapter is the opportunity to build on what Damien and the team have created. The industry is shifting back toward genuine advisor-client relationships and away from product-driven advice. That’s how we’ve always worked, and it’s where we’ll continue to focus.

Daniel Rolley (Chief Investment Officer)

2025 has been another strong year for markets, but the landscape heading into 2026 is becoming more complex. Central banks are starting to diverge on interest rates – the US will likely continue cutting rates, Australia is expected to hold steady and Japan is likely to raise rates. This isn’t the uniform easing cycle we saw in 2025, which means more dispersion and volatility ahead.

Trade tensions have settled somewhat. After earlier tariff backflips, markets have largely stopped overreacting to every headline, taking the view that the tough talk is more negotiating tactic than policy. But risks remain if barriers escalate further. Meanwhile, governments worldwide are spending more on defence, critical infrastructure and energy security, pushing debt levels higher. Gold’s 50% rally this year reflects investors seeking protection against currency devaluation amid mounting fiscal deficits.

AI investment continues to dominate the conversation – and for good reason. Capital investment in US data centres is expected to boost GDP by around 0.5% next year, which is substantial. However, we’re starting to see signs of excess, with some companies now issuing debt to fund AI bets. When debt markets price in a 9% probability of default on some major players, it suggests we may be approaching limits in certain areas.

In 1996, Fed Chairman Alan Greenspan famously warned of “irrational exuberance” in markets. Today might be better described as rational exuberance – there are genuine reasons for optimism, but selectivity remains essential. Established technology leaders like Amazon, Microsoft and Alphabet trade at reasonable valuations and boast strong earnings growth. In contrast, some of the more speculative AI-related names are trading at nearly 100 times revenue – a stark reminder that selectivity matters.

At Financial Decisions, our portfolios remain diversified across international equities, with exposure to Europe and sectors beyond technology including healthcare and industrials. Defensive assets continue to offer attractive yields, from term deposits through to corporate bonds and private credit.

In Australia, we’re favouring mid and small-cap stocks where earnings growth is strongest, rather than the major banks where valuations have become stretched despite limited earnings growth.

Our investment approach remains balanced – participating in growth opportunities while maintaining defensive positions to smooth returns. We believe in being in the market for the long term rather than trying to time it – and we’re here to help you do exactly that.

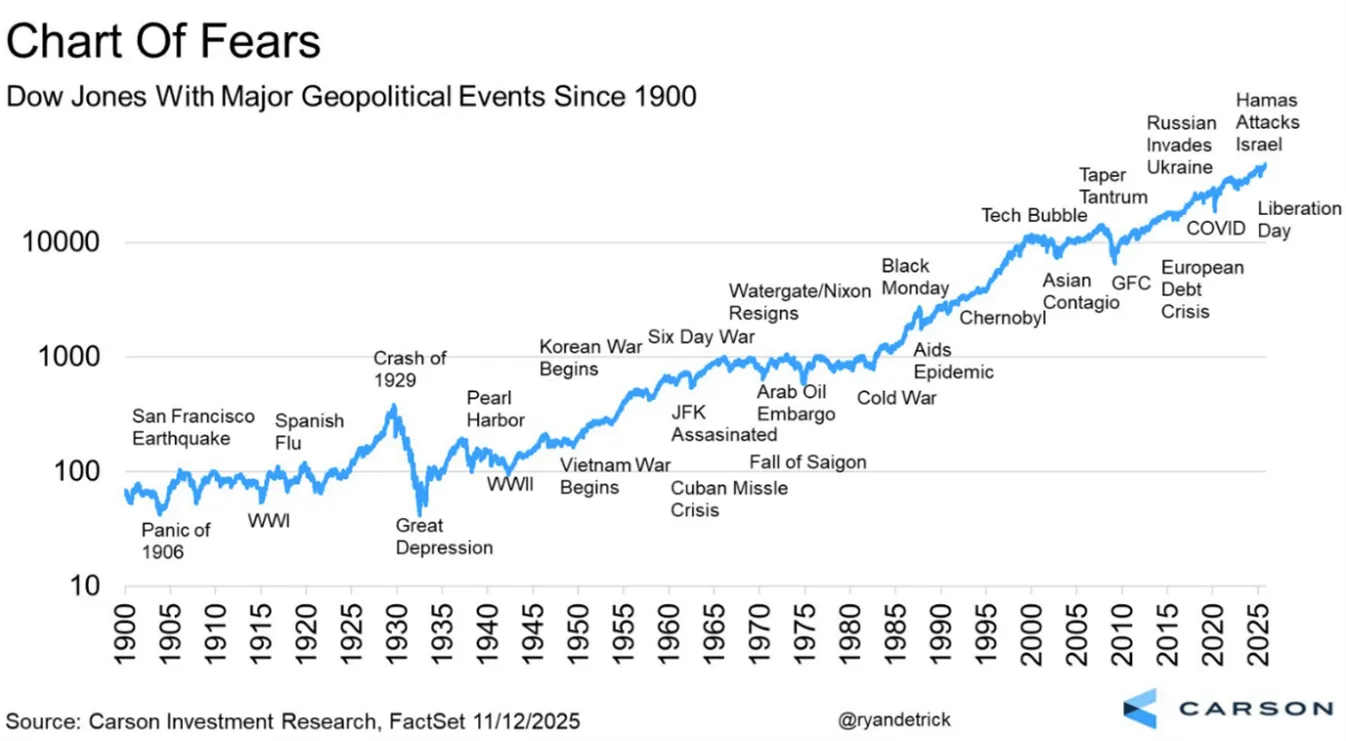

As the chart below shows, markets have climbed through wars, crashes and pandemics. If in doubt, zoom out.

Tim Brosnan (Head of Wealth)

After a relatively soft landing over the past 12 months, the outlook for 2026 is optimistic; however, inflation remains a key variable. After a run of cuts, Australia looks to have reached the bottom of the interest rate cycle, though the US may have further to go.

AI has started to come into its own this year. After a lot of talk, we’re seeing practical use cases in business, and the infrastructure investment – particularly in data centres – has been phenomenal. The scale of these technology giants now rivals medium-sized countries. For investors, the question will be whether AI delivers sufficient productivity gains and cost savings to continue to justify valuations.

Are we in an AI bubble? That’s the million-dollar question, and views differ. Whatever you call it, my view is that valuations will deflate at some point, whether in six months or three years. But this is different from the dotcom boom of 2000. The major technology companies today are making substantial profits, so any correction is more likely to be a pullback than a collapse. I still think there’s room to run. There’s nothing wrong with being in a bubble as long as you’re not the last person in! The key is diversifying assets and not overcommitting during periods of strong growth.

On trade, tariffs have settled into a manageable reality. They grab a lot of headlines but are essentially a tax on foreign goods – and as long as tensions don’t escalate into full-blown trade wars, the impact appears to be sector-specific rather than systemic. Travel and healthcare have felt some pressure, while other sectors remain resilient. Interestingly, Australia is actually exporting more to the US now than before the tariffs were introduced.

Defensive assets like credit funds and term deposits aren’t delivering the returns we saw 12 months ago, as interest rates have come down. However, they’re still offering solid yields and remain an essential part of a diversified portfolio.

Looking ahead, a likely scenario is that Australian rates hold steady while the US continues to ease. If so, that should support international shares while keeping our defensive assets paying reliable income. But with inflation still in play, nothing is guaranteed. If rates rise, valuations would come under pressure, particularly in high-growth sectors.

Peter Lever (Head of Tax & Accounting)

After a decade-long partnership with Financial Decisions, most recently as Acting Head of Tax & Accounting, I’m excited that my team, our clients and I have officially joined the company moving forward. In practice, nothing changes except for having a bigger, more closely integrated team to support you.

Last year, I flagged that the ATO was planning to crack down on compliance, and they’re certainly following through. As of 1 July 2025, the general interest charge on overdue tax is no longer tax-deductible, so falling behind now carries a bigger penalty. Thresholds for PAYG instalments have also been reduced, bringing more clients into regular reporting, and pushing some businesses toward monthly rather than quarterly lodgements. More generally, lodgements need to be on time, payments made or arrangements in place.

On superannuation, the guarantee rate has increased to 12% and the government is pushing for same-day super contributions, meaning super would be paid at the same time as wages rather than quarterly. This is partly aimed at addressing the government’s concerns around unpaid super each year. For business owners, it can help smooth out what can otherwise be lumpy quarterly payments.

Two areas continue to generate questions from clients – and plenty of headlines. Division 296 (the proposed additional tax on super balances above $3 million) remains in flux. The original proposal has been largely scrapped and replaced with something very different, but it’s still not legislated. The idea of broader tax reform is also gaining momentum in policy circles, with talk of lower corporate and income tax rates offset by a higher GST. Nothing is imminent, but be assured we’re closely monitoring these changes and their implications for you.

Finally, the historic intergenerational wealth transfer continues to gather pace. With rising property and living costs, many families are looking for effective ways to support children well before inheritance. If you’re navigating these conversations, we’re here to help with the structuring and tax implications.

All these changes bring risks and opportunities. We invest in intelligent software and training to stay on top of ATO announcements so you don’t have to.

Wade Stanley (Head of Mortgages)

After the prolonged rate holds of 2023 and 2024, this year brought welcome relief for borrowers. The RBA delivered cuts in February, May and August, bringing the cash rate down to 3.60%. For mortgage holders who had been stretching to meet repayments, this easing provided some much-needed breathing room.

Property values have responded strongly. The national average is up 7.5% over the past 12 months, well above the 4-5% annual growth we’d typically expect. Brisbane and Perth have been the standout performers at 12.8% and 13.1% respectively, while Sydney (5.1%) and Melbourne (4.2%) have shown more modest gains.

Supply constraints continue to underpin prices, particularly in the $800,000 to $1 million bracket, where expanded government schemes have opened the door to more first-home buyers.

Looking ahead to 2026, we’re watching closely. The latest inflation data has raised the prospect of a rate increase when the RBA meets in February. For now, our recommendation is to typically stay variable and wait for that data to play out before rushing to lock in fixed rates.

The other significant development is new lending restrictions from APRA, effective 1 February 2026. Banks will be limited in how many high debt-to-income loans they can write – only 20% of their mortgage book can exceed six times the borrower’s income. In simple terms, a borrower earning $100,000 would generally be restricted to a $600,000 loan. The aim is to prevent borrowers from overextending themselves – particularly relevant as five-year fixed loans from 2021 (when rates were around 2%) start rolling off onto today’s higher rates.

While these changes may tighten credit for some borrowers and investors, exemptions apply for loans to buy or build new homes. For most buyers, the immediate impact is expected to be limited, but it’s a clear signal that regulators are keeping a close eye on household debt levels.

As always, now is a good time to review your lending arrangements. Is your current home loan competitive? Have you explored options to leverage equity for investment? Are you considering a property purchase or refinancing in the year ahead? For a confidential discussion about your mortgage or property plans, we’re here to help.

Bring on 2026!

Thank you for your continued trust in Financial Decisions. As we enter this new chapter, we remain committed to helping you and your family achieve your financial goals.

Please note: the Financial Decisions office will be closed for the Christmas period. We wish you a relaxing and enjoyable break.

Disclaimer: This publication has been compiled by Financial Decisions (AFSL/ACL Number 341678). Past performance is not a reliable indicator of future performance. While every effort has been taken to ensure that the assumptions on which the outlooks given in this publication are based on reasonable data, the outlooks may be based on incorrect assumptions or may not take into account known or unknown risk and uncertainties. Material contained in this publication is an overview or summary only and it should not be considered a comprehensive statement on any matter nor relied upon as such. The information and any advice in this publication do not take into account your personal objectives, financial situation or needs. Therefore you should consider its appropriateness having regard to these factors before acting on it. While the information contained in this publication is based on information obtained from sources believed to be reliable, it has not been independently verified. To the maximum extent permitted by law: (a) no guarantee, representation or warranty is given that any information or advice in this publication is complete, accurate, up-to-date or fit for any purpose; and (b) Financial Decisions nor its employees are in any way liable to you (including for negligence) in respect of any reliance upon such information or advice. December 2025

Contact: Financial Decisions PO Box 484 Mona Vale NSW 1660, T 02 9997 4647