Deglobalisation

Over the past few decades, investors and consumers have experienced an era of globalisation. Globalisation undeniably brought about stronger world growth and cross-border trades and efficiency, but there is evidence that the golden years of globalisation are coming to a close. While most retail investors may not recognise it just yet, the long-held notion of globalisation is certainly under “intensive care.” The era of US and European companies moving manufacturing facilities into China due to their low labour costs, and lax labour and environmental laws, are all being challenged and tightened.

While large corporations have started to move out of China to find countries with lower labour costs, the election of Donald Trump as US President certainly gave deglobalisation further traction. Arguably, this is the most anti-China US Government that we have seen in at least a generation. However, Xi Jinping’s China has also been on a path to gain world supremacy in a vast array of areas. Increasing labour costs has enabled their society to be richer and is one part of the equation that has caused us to be at an inflection point. China knows that the process of deglobalisation has started and has been preparing for it. They have been on a course of using its fast-growing middle and upper classes to enable it to sustain a domestic led demand society for their future growth and indeed, economic ascendancy.

Since World War II, the bilateral relationship between the US and China has served both countries well. This relationship has brought about monumental growth in wealth for both countries and also brought China to the No. 2 spot in world economic power for the past decade. However, it seems like we are now experiencing a whole new ball game. Riots in Hong Kong, along with election surprises such as Trump and Brexit, are all examples of this shift in thinking and a changing world – geo-politically, socially and economically. Current and future US political leaders will no doubt have their hands full, wondering just how to best handle a relationship with China that has become more combative in recent times.

We are no doubt beginning to see a world in transition. However, what does a “deglobalising” world potentially look like? Fidelity International recently put out a summary of the potential issues and we highlight this below –

Geopolitics

We could see a world evolving into 3 major supply chain regions – Europe, US-led Americas and a China-led Asia. Trade restrictions (such as through tariffs) could be the start of a drawn-out cold war between the US and China.

Political volatility

We may only have seen the beginning with Brexit and Trump’s election. The rise in political uncertainty could be a rise in market volatility in the future.

High indebtedness

Central banks printing money has supported markets but this has had the effect of widening the gap between rich and poor.

Persistent low interest rates

The unorthodox method of supporting the economy has provided cause for concern for the future law of financial markets. If Governments are able to have negative interest rates on their bonds, zero rates may not be low enough. This could be argued as being both unconstitutional as well as robbery.

Technology

Once touted as the solution to many problems, recent headlines to do with privacy and the impact of Artificial Intelligence (AI), has society believing that it is now more of the problem rather than the solution.

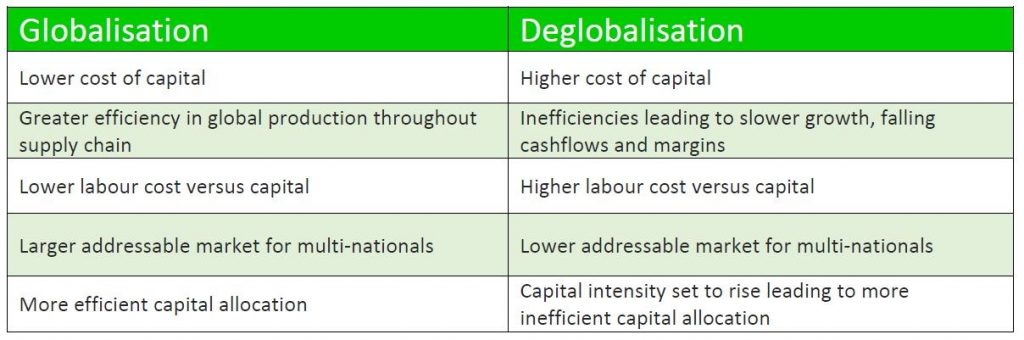

The below table provides a big picture comparison between what we can expect from the impact of this transition to deglobalisation.

A paradigm shift from globalisation to deglobalisation will take time to truly set. This does not mean that we value companies any differently and it certainly does not mean that previous investment philosophies become obsolete. Global investing is still lucrative and continues to provide exposures and important diversification to any portfolio. What it does mean however, is that there could be some unusual market behaviours, more geo-political influence and a widening of the valuation gap between companies that can grow amidst the transition and those that just stay flat or worse, decline.

This valuation and earnings gap could also have some social impact down the road. There will be a larger pool of the super-rich, a growing number of which will be under 40, especially those in technology. The widening gap between society’s rich and poor could also provide impetus for more social unrest and disapproval with Governments around the world. We are already seeing the beginning of these types of occurrences and there is no doubt there are more to come.

If you wish to discuss any concerns about the current market or about any strategies to do with your financial plans, do not hesitate to call your Financial Adviser.

Disclaimer: This publication has been compiled by Financial Decisions (AFSL/ACL Number 341678). Past performance is not a reliable indicator of future performance. While every effort has been taken to ensure that the assumptions on which the outlooks given in this publication are based on reasonable data, the outlooks may be based on incorrect assumptions or may not take into account known or unknown risk and uncertainties. Material contained in this publication is an overview or summary only and it should not be considered a comprehensive statement on any matter nor relied upon as such. The information and any advice in this publication do not take into account your personal objectives, financial situation or needs. Therefore you should consider its appropriateness having regard to these factors before acting on it. While the information contained in this publication is based on information obtained from sources believed to be reliable, it has not been independently verified. To the maximum extent permitted by law: (a) no guarantee, representation or warranty is given that any information or advice in this publication is complete, accurate, up-to-date or fit for any purpose; and (b) Financial Decisions nor its employees are in any way liable to you (including for negligence) in respect of any reliance upon such information or advice. October 2019

Contact: Financial Decisions PO Box 484 Mona Vale NSW 1660, T 02 9997 4647, F 02 9997 7407