As we head into the close of a financial year impacted by the pandemic, interest rate rises, inflation and a federal election, there is a lot to consider in the coming months.

On top of EOFY tax considerations, in this edition of Pulse we explore the latest family trust developments, tips for property investors, how to deal with cryptocurrency gains or losses, why super matters more than ever and how to apply for the Director ID Number.

As always, if you have questions, call our team on (02) 9997 4647.

What Family Trusts Section 100A means for your family

Section 100A is an anti-avoidance provision targeted towards arrangements where a beneficiary is presently entitled to trust income, but where the economic benefit of that income is received by a person other than the presently entitled beneficiary.

For example, consider the scenario where Mum and Dad run their investments through a family trust. The trust generates $80,000 of income in a given year and the distributions are made in equal proportions to four beneficiaries – Mum, Dad, their son and daughter. The children then reimburse or gift their parents back the $20,000 of their share of distributions.

The effect of this arrangement is to reduce tax liability, and if that was the intended purpose then potentially s100A will apply. If s100a applies, then a deeming rule takes effect to ensure that the beneficiaries (the children in this scenario) will not be considered presently entitled to the diverted income. Instead, the trustee becomes liable to tax at the top marginal tax rate i.e., 47%.

The concerning part relating to s100A adjustments is that there is no limited amendment period in relation to the assessments that may be made pursuant to this section of the Act. Given the scope of application of this measure and potentially significant financial detriment, this is very much a live issue for many of our clients.

How can you reduce the risks? There are a range of appropriate measures and strategies that we can help you with, for example reviewing prior year distributions. If this issue potentially impacts you, it is important to consider the implications immediately to mitigate the potential downside.

Tax tips for property investors in an inflationary market

Faced with an extended period of rising interest rates and inflation, now is the time to reassess and adjust your property investment strategy.

Recent changes mean that expenses such as travel to inspect your property are no longer deductible. When prepaying expenses ensure to draw a distinction between what the ATO considers to be a repair and what is an improvement, as improvements may not be deductible and will only add to the cost base of your property. If you have recently entered the investor market, then consider taking out a depreciation report for your investment property.

More importantly, what is your strategy with rising interest rates and potential changes in house prices? Consider pre-paying your interest on property investment loans if there is sufficient cash flow to claim an immediate tax deduction.

If you are intending to renovate and flip a property, it is imperative to understand that renovations of a property with the intention of selling it for a profit in the short term could have significant GST implications.

The ATO and cryptocurrency investing / trading

Did you know that the ATO has access to data obtained directly from digital currency exchanges? It is important to understand the tax treatment on any income or losses you derive from trading in cryptocurrency assets. As an emerging area, the tax treatment around this asset is not so straightforward and to some extent will depend on your individual circumstances.

Some investors will end up with capital gains or losses from their crypto transactions, while others may end up with income tax gains or losses. At Financial Decisions we are across the latest changes, and a five-minute discussion around the best way to go about dealing with your current or planned cryptocurrency transactions could save you a lot of hassle, and money, in the long run.

The importance of super for wealth creation and tax optimisation

Whether you’re employed or a business owner, the importance of our superannuation system as part of your wealth creation and tax optimisation plan cannot be understated.

Here are five reasons and considerations that you may want to prioritise as part of your super strategy:

- Superannuation provides for a concessional tax environment whereby any investment earnings are taxed at a maximum rate of 15%.

- Compounding returns over the years is key to building long-term wealth.

- Subject to your eligibility and transfer balance caps you may want to consider starting an account-based pension (ABP) – for those in pension mode the tax rate on investment earnings within the fund is zero.

- Recent legislation changes mean that you can have six members in your SMSF, which means larger families can share a single superannuation fund to potentially spread operating costs across more members. Plus, new members can inject new funds into your SMSF and help meet liquidity issues such as minimum pension requirements for those funds that hold mainly illiquid assets. Extra funds could potentially also assist in limited recourse borrowing arrangements.

- Your SMSF is more likely to be considered an Australian Superannuation Fund in the event where one or more members may travel overseas for an extended period.

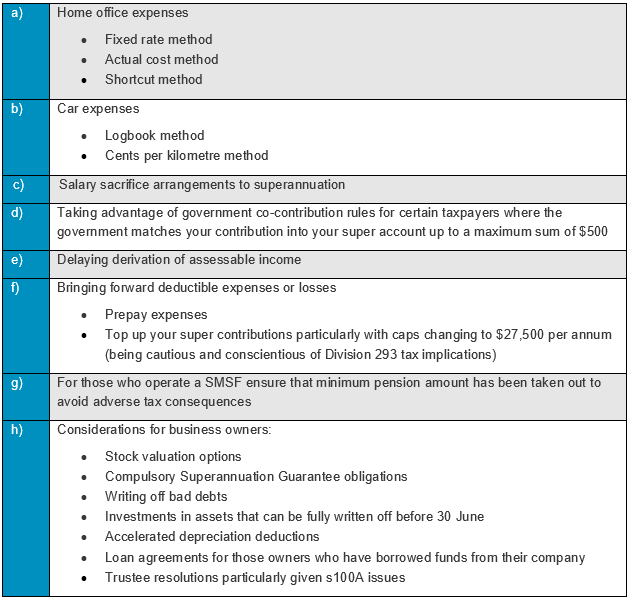

Checklist: EOFY tax considerations to discuss with your adviser

With 30 June just around the corner, it’s time to make sure you get all your ducks in a row to optimise your tax position. The following points should ideally form part of your end of year tax planning and discussion with your adviser:

Update: Apply for your Director ID Number by 30 November

In our previous Pulse newsletter we spoke about the Government’s decision to bring in Director Identification Numbers for all directors of a company. Please be reminded that all directors of companies currently in operation are required to apply for the Director Identification Number by 30 November 2022.

The fastest way to apply is through the MyGovID app. Alternatively, you can call the Australian Business Registry Services to arrange a paper application. Under the regulations, only the director themselves can apply for the Director Identification Number. Learn more and apply online at MyGovID.

We’re here to help

Financial Decisions is here to offer a single point of contact for our clients to manage their financial, business and legal affairs across all stages of their professional and personal lives.

If you have any questions on these issues or need advice, please call us on (02) 9997 4647.

Contact: Financial Decisions PO Box 484 Mona Vale NSW 1660, T 02 9997 4647, F 02 9997 7407