Smart Strategies to get into Prime Position

With just one month remaining in the financial year there is, as always, a great deal of attention being given to tax. Often placed on the backburner of financial strategies, this is the time of year when most people realise they have potential gains – or losses – that impact their economic situation, and tax becomes appreciated as the key to a happy new financial year.

June is also the perfect time to track the impact of the strategies you implemented throughout the financial year. In the last edition of PULSE (November 2017) we discussed some blueprint actions that can provide serious assistance in establishing not only the best tax position possible, but also optimising your wealth creation and management tactics.

If you implemented any of these initiatives, the results achieved are a great indicator of how to structure your financial plan from a tax perspective for the upcoming financial year – and for how you will fare once 30 June rolls around.

In building upon those strategies and reviewing how successful they have been for you, we return to following factors that were raised in our prior edition of PULSE:

Mortgage and Debt Optimisation:

Non-deductible debts can be painful in the extreme. Perhaps chief among these, mortgages are a considerable non-deductible debt frequently dominating many individuals and family’s personal economies. It is important to identify whether the balance of any of your non-deductible debts has changed and what specific effects this will have.

If you have made additional contributions in reducing the debt throughout the year, this could have a range of implications in terms of ensuring debt optimisation, so it is certainly worthwhile investigating. When reviewing your mortgage, it is imperative to ask whether the interest rates on your loan are helping or hindering your situation – especially given that the current going rate is sitting at around 3.63%.

Investments:

Interest rates should be of a fundamental concern for those with investment properties. In certain circumstances, investors can also realise the reduction of their rates to as low as 3.63% despite it being an investment and not a primary residence. Refinancing could result in additional funds being freed up to enhance your cash flow and / or pursue other financial objectives.

In the event that your investments have brought about any significant capital gains, you have the potential to offset them against investments with minimal future potential that are currently drawing a negative net result for you. One tactic here might be to reset your cost base for the securities that will result in any capital gains through the sale of that stock prior to 30 June, thereby, taking profits as they stand with minimal capital gains impact since the gains would be offset against any realised losses and then purchasing that same stock post 30 June, albeit at a higher price.

Superannuation:

Given the recent changes to the superannuation environment, questions may be asked whether super is still considered to be an effective wealth creation and/or wealth preservation strategy. Short answer is Yes. It is still a prime means of creating wealth for the future and enhancing your current situation. Ensuring that you have maximised use of the amended caps can provide stability and go a long way towards future-proofing your retirement.

For those operating an SMSF please ensure your minimum pension payments for the year have been met. With the federal government last year revoking the 15% exemption on fund earnings for those who have a TRIS (transition-to-retirement income stream), it is prudent to devote careful deliberation as to whether to continue drawing a pension from your fund. As always, knowledge is power, and being aware of options and alternatives will help inform your future tactics for managing your wealth.

Upcoming Change:

Property Developers – New GST withholding measures commence on 1 July this year. The broad effect of these measures is withholding of GST following the sale of new residential premises or new subdivisions. The rate of withholding is 7% of the applicable price if the margin scheme applies or 10% otherwise. Get in touch with your solicitors to understand the process moving forward.

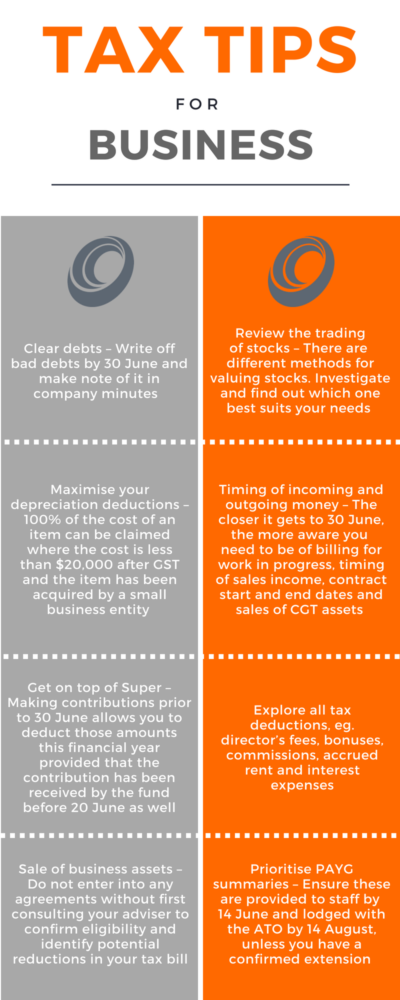

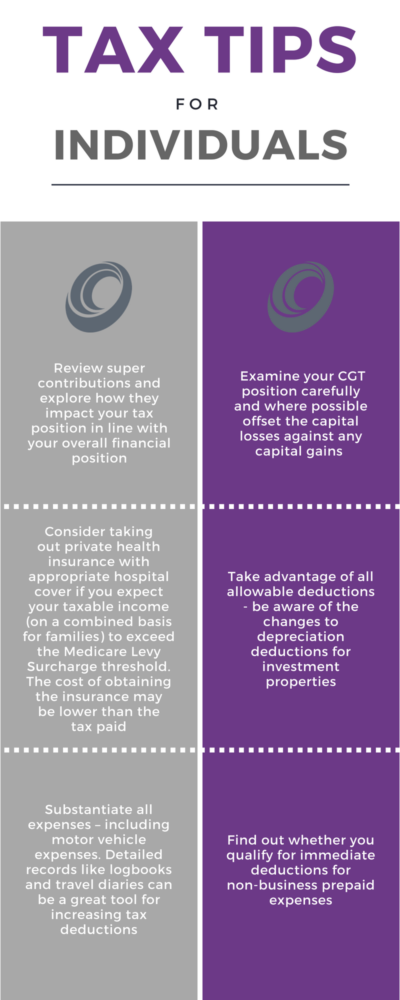

Tax Tips

From personal income through to business tax, enhancing your financial situation through effective navigation of concessions and returns is not as hard as it seems. Here are some straight forward considerations that could enhance your taxation position, and ensure you stay on the right side of the ATO!

American Tax Reform

What it means for our clients who are dual citizens

With the sixth largest population of Americans living outside of the USA, recent changes to tax practices and legislation mean that many expats and dual citizens may have to pay tax on superannuation, accruals and distributions made in Australia.

This effectively creates a double taxation situation of Australian superannuation funds, despite a complete lack of any American connection to the funds whatsoever outside of the policy holder’s US citizenship. This has created a climate in which many expats are faced with weighing up whether their sentimental attachment to their US citizenship justifies the enormous financial consequences they have and will continue to experience because of it.

In the last year alone, the IRS has launched 13 new international tax compliance programs that are having an impact on both expats and Australian businesses with US connections. Plus, with these international reforms to US tax law, tax cuts in the US and the Jobs Act 2017, things are likely to get worse economically for US expats.

Being one of the only countries that applies taxes to the international income and estate of its citizens, the burden of filing and paying US tax on Australian earnings is substantial. However, quite confusingly, while the classification of super funds under US domestic tax laws and the tax treaty is deemed a fully taxable asset of the US expat, ALL contributions, earnings accrued and distributions from a super fund to the expat are more than likely NOT subject to current US taxation law.

Recent provisions have introduced the concept of a “one-time transition tax” to be instituted on the deferred foreign income of a foreign corporation. The relevance of this for expats is that the tax is payable by US citizens who own a controlled foreign company (CFC) or at least 10% value in a foreign corporation that does not qualify as a passive foreign investment company.

US expats who are members of a SMSF that has a corporate trustee will be also be subject to this CFC classification, along with family discretionary trusts with US member beneficiaries that qualify for business or investment trust treatment under American tax regulations.

The tax, as described by Dungog and Berg of Moodys Gartner Tax Law:

“is imposed on the deferred foreign income of such a foreign corporation which constitutes aggregate post-1986 earnings and profits (deferred earnings) as determined under the US tax laws. The deferred earnings measurement date is the greater of 2 November 2017 or 31 December 2017, depending on which of the two dates produces the higher balance of deferred earnings. The tax is imposed at different rates – the individual shareholders have a higher transition tax rate than corporate shareholders, specifically, 17.5% rate of tax cash assets and 9% of non-cash.”

The upshot of this is that all US citizens living outside of America who fall under this new system will need to pay this one-time transition tax, with the option of doing so in a lump sum or installments over a period of eight years.

All this begs the question; perhaps it’s time for US expats to put sentiments aside and consider renouncement of their US citizenship.

Ref: Dungog, Marsha-laine F. (US Tax Lawyer), Berg, Roy A. (US Tax Lawyer), Moodys Gartner Tax Law. The impact of US tax reform provisions on Australian Super.

Helping you get the Most out of Tax

It is not all about tax but about your overall financial health - we are here to support you every step of the way. Get in touch with Chetan Sharma or your adviser and we’ll help take the sting out of tax time and make progress towards realising your financial goals.

Contact: Financial Decisions PO Box 484 Mona Vale NSW 1660, T 02 9997 4647, F 02 9997 7407