Welcome to the September edition of our Exchange Newsletter.

In this edition, we bring you highlights from the US reporting season, discuss impending changes to income protection insurance, show you how to save thousands by refinancing your mortgage, and outline four government assistance schemes to help first home buyers purchase a new property.

We’ve also included a link to a video that features our Chief Investment Officer, Daniel Rolley, with an introduction from our Head of Wealth Management, Archana Bhatia. As part of a series that analyses key market trends and their implications on investment, this first video discusses the US reporting season, the Chinese technology sector, and key sectors within the Australian share market. Click on Daniel’s image below to watch.

Daniel Rolley

Chief Investment Officer

Happy reading…and viewing!

US Reporting Season Highlights

The latest US quarterly reporting season has drawn to a close, with many companies achieving record profit margins despite rising input costs from raw materials and wages. This is largely thanks to COVID-19 related cost savings (e.g. rent abatement, wage subsidies), as well as passing on costs to their customers. This is particularly the case for larger companies with strong pricing power and strong balance sheets in sectors with only one or two dominant players such as technology and communications. We believe that investors positioned in these types of companies will continue to benefit over the long-term.

Many of the highlights have come from the technology sector, which is a beneficiary of structural trends such as restrictions on movement for individuals and businesses due to COVID-19. Microsoft and Alphabet (Google) are the two most notable beneficiaries of these trends, and despite their enormous size, have grown their revenues by 21% and 57% respectively in the past quarter. We expect these companies will continue to be supported over the next decade as consumers increasingly use their software and platforms to do business and reach customers more efficiently.

One of our preferred sectors is healthcare, which continues to benefit from ageing populations and increasing per capita expenditure on healthcare products and services. Johnson & Johnson (JNJ) is the world’s largest healthcare company, with operations spanning pharmaceuticals, medical devices and consumer products. JNJ posted a strong quarterly result with sales increasing by 24%. This was driven by the strength of its Board, as well as its medical devices business (sales +57%), which is leveraged to re-opening of hospital procedures such as orthopedic (hip and knee) operations. We believe JNJ is one of the most reliable ways to invest in these favourable long-term trends.

COVID-19 has negatively impacted the industrial complex over the last year as supply chains were disrupted across a range of sectors. This disruption reinforces the need for supply chains to increase spare capacity (moving from ‘just in time’ to ‘just in case’) and increase efficiency through automation. We have several companies in our Model Portfolios that are leveraged to these trends, including US-listed firm Rockwell Automation (ROK). Globally diversified and covering industries such as semiconductors, automotive, food & beverage, life sciences, and chemicals, ROK provides automation solutions that increase operational efficiency from control systems through to analytics. ROK increased their sales by 32% in the last quarter and closed the quarter with record levels of forward orders.

Not all results were greeted with investor cheer, particularly companies that performed strongly over the past year but are now seeing slowing growth trajectories. This includes businesses leveraged to eCommerce such as PayPal (sales +18%) and Amazon (sales +27%). Both firms continue to see double digit sales growth going forward, however at lower rates than in the past year. In our view, any protracted share price weakness is an opportunity to add to some of the best global businesses with a long runway of growth in the years ahead.

Impending Changes to Income Protection Insurance

Protecting your future earning capacity is as important, if not more important, than protecting your home.

Income protection insurance can provide much-needed funds in the event that you suffer a serious illness or injury and can’t work for an extended period of time.

Sweeping changes to income protection insurance policies are due to come into effect in October 2021, with some already in place. The changes are a result of the insurance regulator intervening in the industry to address substantial and unsustainable ongoing losses on these policies.

Here are the major changes aimed at reforming the industry:

‘Agreed Value’ income protection policies to be abolished

Agreed Value policies refer to policies where the monthly insured amount is agreed at the start of the policy without needing to prove what you were earning at the time of claim. This type of policy provides additional security for self-employed individuals whose annual income may fluctuate. However, since 31 March 2020, insurers have not been allowed to offer Agreed Value income protection policies to any new clients (they can still uphold existing policies). All new policies are to be based on an Indemnity Value, where the value of the claim paid is based on your income in the past year or two years, depending on the terms and conditions of the policy.

Removal of ‘guaranteed renewable’ on new policies

Currently, insurers guarantee that policies will be renewed each year for at least the same level of cover and under the same (or improved) terms and conditions over the contract period (e.g. to age 65), providing you continue to pay your premiums on time. However, from 1 October 2021, insurers will no longer be able to offer policies that are ‘guaranteed renewable’. Instead, policies will be subject to a review of your income, occupation and the generosity of the terms and conditions of your policy every five years. This means the insurer may decide to change the terms and conditions you need to satisfy to make a claim after the five year period, however the contracts can be renewed without medical reviews for further periods (not exceeding 5 years). Existing policies entered into prior to 1 October 2021 will continue to be guaranteed renewable for the life of the policy.

Stricter rules around disability claims and cover

From 1 October 2021, the regulator expects insurers to incorporate design features into their products to control risks associated with longer-term policies (such as to age 65). An example is stricter disability definitions, including moving from a three-tiered definition of disability (duties, hours, income) to a one-tiered definition based only on important duties. Further examples include reducing the income replacement ratio after a specified period of time on a claim or adopting a stricter ‘any occupation’ definition after an initial ‘own occupation’ two year benefit period. Insurers are currently in the process of developing new policies in line with these changes.

Is your future earning capacity protected?

If you don’t have income protection insurance or you wish to increase your cover, now is an opportune time to apply in order to gain the benefits of guaranteed renewability and more favourable policy definitions before sweeping changes come into effect on 1 October 2021.

For more information about the proposed changes or income protection insurance in general, please contact your adviser.

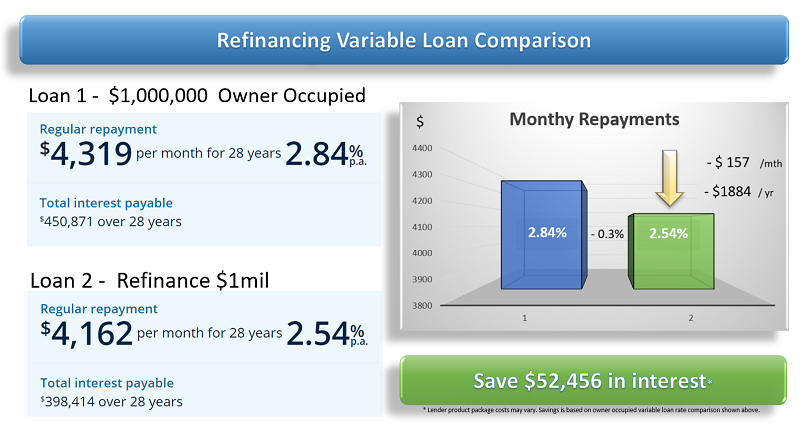

Does your Mortgage need a Health Check?

With record low interest rates prevailing, now is the time to look around for an even better deal on your home loan. Refinancing your mortgage to a lower interest rate can save you tens, if not hundreds of thousands of dollars over the life of the loan. Potential savings are shown in the loan scenario below.

Loan scenario

- You purchased an owner occupied property for $1,3000,000 two years ago.

- You financed the purchase with a 30 year P&I loan of $1,040,000 at a variable rate of 2.84%.

- After two years, you still owe $1,000,000 with 28 years left on the loan.

Ready to save thousands on your mortgage?

Wade Stanley

Mortgage Adviser

Contact us today about refinancing your mortgage and let us do all the hard work for you.

Call our Mortgage Adviser, Wade Stanley, on 0415 993 444.

Government Assistance for First Home Buyers

Despite interest rates remaining at record lows, the dream of owning property seems further away than ever for many first home buyers. Thankfully, there are a number of government initiatives available to help first home buyers get a foothold in the property market.

First Home Deposit Scheme (FHLDS)

- All 5,000 spots released on 1 July 2020 have been filled

- An additional 10,000 spots will be available from 1 July 2021 to 30 June 2022

- Home buyers can go onto the wait list (self-registration online)

- Family Home Guarantee gives eligible single parents with dependents the opportunity to build a new home or purchase an existing home with a deposit of only 2%

- More information at: https://www.nhfic.gov.au/what-we-do/fhlds/

First Home Super Saver Scheme (FHSSS)

- Self-registration online or via your accountant

- Apply to release your voluntary super contributions

- Maximum $15,000 per year (total $30,000)

- Proposed changes to $25,000 per year (total $50,000)

- More information at: https://www.ato.gov.au/individuals/super/withdrawing-and-using-your-super/first-home-super-saver-scheme/

First Home Owner Grants (FHOG)

- $10,000 grants available for first home buyers that are buying or building a new home

- More information at: https://www.revenue.nsw.gov.au/grants-schemes/previous-schemes/first-home-owner-grant

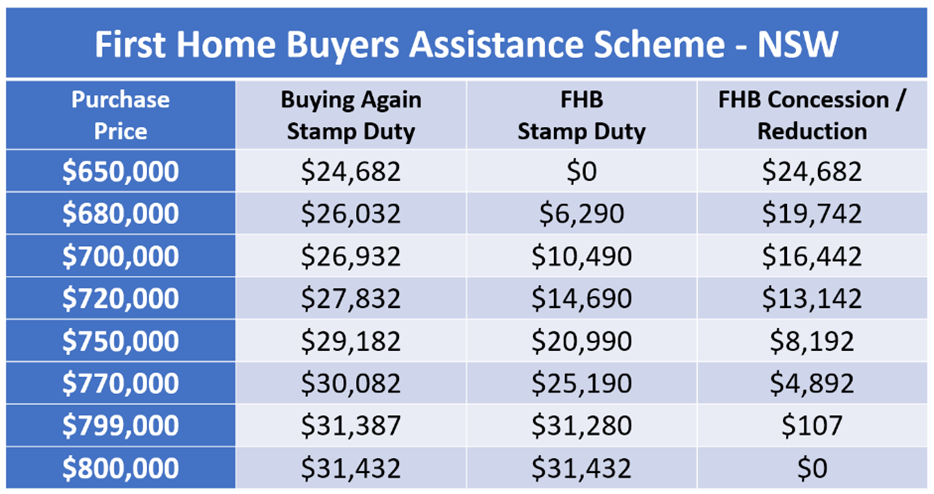

First Home Buyers Assistance Scheme (FHBAS)

- First home buyers may be eligible for stamp duty reductions on existing dwelling purchases (see table below)

- More information at: https://www.revenue.nsw.gov.au/grants-schemes/first-home-buyer/assistance-scheme

We’re Here for You

If you would like assistance with any aspect of your wealth creation and management strategies, please contact your adviser directly or feel free to call us on (02) 9997 4647.

Disclaimer: This publication has been compiled by Financial Decisions (AFSL/ACL Number 341678). Past performance is not a reliable indicator of future performance. While every effort has been taken to ensure that the assumptions on which the outlooks given in this publication are based on reasonable data, the outlooks may be based on incorrect assumptions or may not take into account known or unknown risk and uncertainties. Material contained in this publication is an overview or summary only and it should not be considered a comprehensive statement on any matter nor relied upon as such. The information and any advice in this publication do not take into account your personal objectives, financial situation or needs. Therefore you should consider its appropriateness having regard to these factors before acting on it. While the information contained in this publication is based on information obtained from sources believed to be reliable, it has not been independently verified. To the maximum extent permitted by law: (a) no guarantee, representation or warranty is given that any information or advice in this publication is complete, accurate, up-to-date or fit for any purpose; and (b) Financial Decisions nor its employees are in any way liable to you (including for negligence) in respect of any reliance upon such information or advice. September 2021

Contact: Financial Decisions PO Box 484 Mona Vale NSW 1660, T 02 9997 4647, F 02 9997 7407