Welcome to our third edition of Exchange for 2020. It’s been a strange and trying year for many people and we certainly hope that you and your family remain well.

In this edition, we examine the insurance industry and how Income Protection losses across the industry have been going on for many years. Unfortunately this has repercussions and many of you with Income Protection cover will likely have changes made to your policy or a rise in premiums.

On an upside however, we also look at new initiatives for mortgages, in particular, a number of opportunities for first home buyers, recently announced by the NSW Government.

Changes to Income Protection Policies

The insurance industry has been the subject of intense scrutiny, especially since the recent Royal Commission, and is currently going through a period of rapid change. A large part of this can be attributed to issues surrounding the profitability of Income Protection.

As a result, some new or existing policyholders may find Income Protection (IP), in its current form, is becoming too expensive. However, it is not just premiums that are affected. There has also been the elimination of Agreed Value premiums for IP. The Australian Prudential Regulation Authority (APRA) has ruled that insurers will only be allowed to offer policies where the benefit amount is based on the policyholder’s income at the time they make a claim.

This is as a result of insurance companies offering large discounts in order to gain market share, following an absence of industry cohesion. The industry made a net loss after tax of $1.6 billion over the 12 months to June, a “significant reduction” from the previous year’s $438 million profit.

APRA has mandated that the industry moves to making services more sustainable for the income protection market. Unfortunately this is occurring during the COVID-19 pandemic, a period in which the insurance companies are getting overwhelmed with claims. It is also expected that mental health claims are to increase in the months and years ahead from the effects of the COVID-19 pandemic. The end result is that premiums have to rise for life insurers to achieve profitability and to continue to meet their claim obligations.

Some changes that may be made to your existing IP cover to reduce premiums include:

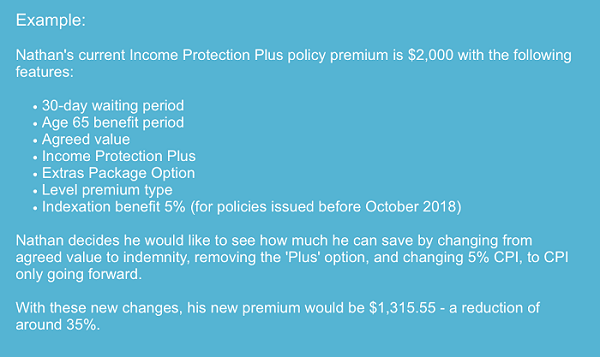

- A change from Income Protection Plus to Income Protection Standard: You must be completely disabled for 14 of the initial 19 days in the waiting period, and completely or partially disabled for the remainder. Offsets include any payment received as a result of worker’s compensation or accident claim, or claims made from social security benefits.

- A change from Agreed Value to Indemnity: Your monthly benefit will be the lesser of 75% or 60% of your pre-disability earnings, and the insured monthly benefit amount. There is a possible premium reduction of 25%.

- A change from Indemnity 75 to Indemnity 60: Your secured monthly benefit amount can replace a maximum of 60% of your pre-disability earnings, instead of the previous 75%. This shows an approximate 9% premium reduction and reduced monthly benefit.

- Removal of the Extras Package Option: You will no longer be covered for the following benefits – Trauma, Overseas Assist, Specific Injuries, Family Support, Home Care, Bed Confinement. This may reduce your premium by up to 12.5%.

- Removal of the Increasing Claim Option: The amount you are paid while on Income Protection claims will not increase with yearly inflation, showing a possible premium reduction of 20%.

- Removal of Accident Option: Insurance companies will no longer pay you 1/30 of the Total Disability Benefit for each day during the waiting period for which you are completely disabled as a result of the accident, giving an approximate premium reduction of 5%.

- Changes to the age 70 benefit period: Your income protection will now expire when you reach age 65 at the policy anniversary. Your premium may reduce by up to 10%.

However, there are always options to consider if you are unhappy with your current cover.

- For those who have lost the ability to have an Agreed Value premium/policy, there is the option for you to move to a newly introduced Indemnity 60 benefit type. It has been designed to be an alternative to the existing indemnity policies and the previous Agreed Value policy. It is a suitable option if affordability is an issue yet you require comprehensive cover, or if some self-insurance is possible due to a strong financial position.

- The removal of ‘Plus’ packages on your cover will reduce your premiums, but will require careful consideration.

Move to another insurance company. Making the move from your insurer to another may not be recommended, but you are welcome to discuss it further with us.

As renewal statements are released, and you become aware of any changes to your policy or premium payment increases, we encourage you to give us a call so we can discuss your options and which course of action will work best for you.

Mortgage Initiatives

First Home Buyers Assistance Scheme

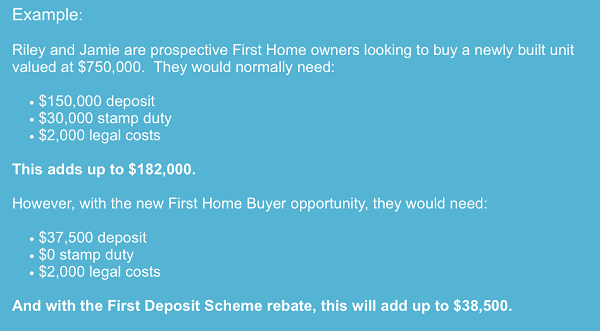

The NSW Government announced on 27 July 2020 that eligible first home buyers may be able to access stamp duty exemptions on new home purchases.

- New home builds will see discounts on stamp duty available for purchases between $650,000 and $800,000 the discount reduces with the increasing purchasing price, phasing out at $1 million.

- The threshold of charged stamp duty on vacant land will also rise from $350,000 to $400,000, discontinuing at $500,000.

To be eligible for a reduction or exemption in the amount of stamp duty payable, you will need to be a first home buyer purchasing:

- a newly built home

- or a vacant block of land on which you intend to build a new home.

For a full exemption to apply, the value of the new home must be no more than $800,000 and the vacant land value must be no more than $400,000.

This is a temporary policy, in place for 12 months and will apply to contracts executed from 1 August 2020 to 31 July 2021. These changes are a component of the NSW Government’s COVID-19 Recovery Plan, aiming to support the property and construction industry which is essential to keeping jobs and investment in NSW.

Government First Deposit Scheme

The government’s First Home Loan Deposit Scheme, introduced on 1 January 2020, is designed to allow better access to the property market for first home buyers. The scheme allows first time buyers to pay a deposit of as little as 5% and to avoid lenders mortgage insurance (LMI). The majority of banks and lenders require a minimum deposit of 20% of the property’s value for the borrower to have an exemption from LMI, however, first home buyers who are unable to reach this threshold under this scheme are able to take out a loan if they’ve saved at least 5% of the property value.

In order to verify your eligibility, you must apply to the National Housing Finance and Investment Corporation (NHFIC) and if you are approved, the government will act as your guarantor when you take out a home loan with a lender – the lender will do normal checks on your financial situation, but this scheme makes it easier to get a loan without having saved for a 20% deposit. The scheme is available for individuals who earn up to $125,000 per annum, and couples with a combined earning of up to $200,000. In order to be eligible, first home buyers must show they have saved at least 5% of the value of the property they are purchasing.

The risk involved with taking out a loan with a smaller deposit is that the amount left owed to the lender is going to be larger. This means that a mortgage taken out under the government’s scheme could make it more difficult for borrowers to repay a home loan.

Note that FY2019/20 notices of assessment are now required for all current and future 14-day reservations to be able to progress to a pre-approval.

Family Pledge Loans

Family Pledge Loans, also called family guarantee home loans and guarantor home loans, are a type of mortgage that allow you to use the equity in a family member’s property as security on your loan when you don’t have a sufficient amount saved for a deposit. Guarantors are limited to immediate family members such as siblings, parents, and grandparents.

Most loans will require the borrower to pay a minimum deposit upfront. This is usually around 20%, less if you pay LMI. With a family pledge you may be allowed to borrow more money whilst providing less of a deposit. Borrowing more than 80% of the property’s value would normally require taking out LMI, but a family pledge will allow you to avoid this extra expense. Additionally, most lender products enable the guarantee to be applied to the 20% deposit only. Once owner equity reaches 80%, the guarantee may be released.

A disadvantage of this plan is, as guarantor, your home may be at risk. Prior to applying for a family pledge loan, it is recommended that you seek financial and legal advice so you are aware a of the liabilities held by the guarantor and the borrower.

Interest Only Loans

With an interest only loan, your repayments only have to cover the interest on the amount you borrowed for a set period. During this period, you pay nothing from the amount borrowed so it does not reduce. At the end of the interest-only period, you’ll start repaying the amount borrowed on top of the interest.

The lower payments during the interest-only period may help you pay off other debts or save money. You could also claim higher tax deductions from an investment property if you are an investor. However, the interest rate may be higher than on a principal & interest loan, and your repayments will increase after the interest-only period. An interest only loan may put you at risk if there’s a market downturn or your circumstances change, and if your property doesn’t increase in value as you will not build up any equity.

To find out more, please call our Mortgage Adviser, Wade Stanley, on 0415 993 444.

Wade Stanley

We’re Here for You

If you would like assistance with any aspect of your wealth creation and management strategies, please contact your adviser directly or feel free to call us on (02) 9997 4647.

Disclaimer: This publication has been compiled by Financial Decisions (AFSL/ACL Number 341678). Past performance is not a reliable indicator of future performance. While every effort has been taken to ensure that the assumptions on which the outlooks given in this publication are based on reasonable data, the outlooks may be based on incorrect assumptions or may not take into account known or unknown risk and uncertainties. Material contained in this publication is an overview or summary only and it should not be considered a comprehensive statement on any matter nor relied upon as such. The information and any advice in this publication do not take into account your personal objectives, financial situation or needs. Therefore you should consider its appropriateness having regard to these factors before acting on it. While the information contained in this publication is based on information obtained from sources believed to be reliable, it has not been independently verified. To the maximum extent permitted by law: (a) no guarantee, representation or warranty is given that any information or advice in this publication is complete, accurate, up-to-date or fit for any purpose; and (b) Financial Decisions nor its employees are in any way liable to you (including for negligence) in respect of any reliance upon such information or advice. September 2020

Contact: Financial Decisions PO Box 484 Mona Vale NSW 1660, T 02 9997 4647, F 02 9997 7407