Estate Planning:

A Worthwhile Investment in your Loved Ones

Many people operate under the assumption that having a will means their loved ones will be looked after and benefit from a lifetime of hard work and shrewd investment strategies.

Many people operate under the assumption that having a will means their loved ones will be looked after and benefit from a lifetime of hard work and shrewd investment strategies.

However, as with all things involving financial planning, the truth is quite different to the perception.

By investing a little time now, the benefits your loved ones derive in the future will be greatly enhanced – and you can be confident that your hard-earned assets will be distributed in accordance with your wishes.

To help take the stress out of the equation, we have provided a few key elements below to consider when planning your estate

Will Alone is not Enough

Traditionally, a will is thought of as being a binding document, setting out to the letter how much and to whom your assets will be appointed once you have passed on. Despite this not being accurate, a well thought out will is a paramount step towards achieving the goals you set for the legacy you want to leave behind.

While a will is a legal document, it alone does not ensure that your wealth is distributed in line with your plans or wishes. It needs to be bolstered by other mechanisms and align with other supporting practices for complete peace of mind for the future.

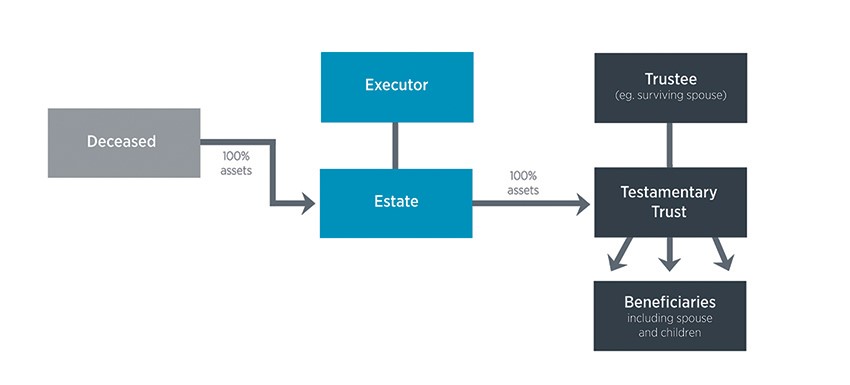

A Testimonial for Testamentary Trusts

Right off the bat, there are three strong arguments for including a testamentary trust in your will:

- Enhanced flexibility in terms of planning and execution.

- Asset protection, both in general and from third parties (eg. creditors).

- Tax minimisation to ensure more of your wealth ends up with your beneficiaries, and less of it ends up in government coffers.

A testamentary trust arises upon your death and, importantly, the trustee has discretionary power to distribute your wealth between a group of beneficiaries nominated in your will under this structure.

This means that the trustees in your will have a greater breadth of options when it comes to managing – and ultimately maximising – what you are leaving behind for them.

The Enduring Power Struggle within the Powers of Attorney

A common misconception is that allocating someone with power of attorney gives them overarching control of your assets and their distribution. What it actually does is authorise someone else to manage your assets and financial affairs in the event that you are unable to do so – whether due to physical or mental incapacitation, or simply due to your absence.

In allocating power of attorney, the nominated person is to act in accordance with the specifications made in your will. This extends to all decisions, such as selling real estate, assets and shares on your behalf as well as administration of bank accounts and tending to bills and costs.

What many do not know is that there are in fact two types of powers of attorney – general and enduring. Enduring power of attorney differs from general power of attorney in that decision-making authority on your behalf does not cease if you become physically or mentally incapable of managing your affairs.

Ensuring Pedigree with Direct-Descendant Trusts

The classic estate planning horror story: someone enters a new relationship after the death of a spouse, changes their will to reflect allocation of resources to their new partner, and upon death the children from the first relationship are left with nothing.

At the core of a direct-descendant trust is the protection of capital flow to your direct descendants. Under the terms of standard wills, you leave assets directly to individuals such as your spouse (if they survive you) and your children.

While the specific people you desire to benefit have been nominated, a standard will does not protect or preserve your assets in the years to come. If the people identified in your will subsequently divorce, separate or go through some form of financial misadventure, those assets are at risk of being severely diminished or, in the worst case scenario, lost altogether.

The basic framework of a direct-descendant trust is such that:

- the flow of the assets is limited to the will-maker’s direct descendants;

- distribution of assets can encompass a broader range of beneficiaries at your discretion, including in-laws; and

- assets are safeguarded from attacks (including from personal creditors and the Family Court) against beneficiaries.

Future-proof your Estate with Succession Planning

With a solid structure and strong administration, succession planning can help achieve a range of objectives for your estate. Primarily, they support trusts and add additional layers of asset protection, tax efficiency and commercial flexibility.

Under a succession plan, trusts within your will form what can be described as a general estate. This means that you effectively do not “own” the trust assets and they do not constitute a portion of your personal estate. Rather, trusts under a succession plan can be viewed as a pool of capital that can be managed at the discretion of beneficiaries – who in effect become shareholders in your estate.

Putting it all Together

Every investment decision has an impact on what you leave behind and one of the best investments you can make is spending time and effort into your estate plan.

Enjoy your life and let us take care of the details. For help, advice or support in planning your estate, contact us on (02) 9997 4647.

The Lighter Side of Money

“Another good thing about being poor is that when you are 70 your children will not have you declared legally insane in order to gain control of your estate.” – Oscar Wilde

Disclaimer: This publication has been compiled by Financial Decisions (AFSL/ACL Number 341678). Past performance is not a reliable indicator of future performance. While every effort has been taken to ensure that the assumptions on which the outlooks given in this publication are based on reasonable data, the outlooks may be based on incorrect assumptions or may not take into account known or unknown risk and uncertainties. Material contained in this publication is an overview or summary only and it should not be considered a comprehensive statement on any matter nor relied upon as such. The information and any advice in this publication do not take into account your personal objectives, financial situation or needs. Therefore you should consider its appropriateness having regard to these factors before acting on it. While the information contained in this publication is based on information obtained from sources believed to be reliable, it has not been independently verified. To the maximum extent permitted by law: (a) no guarantee, representation or warranty is given that any information or advice in this publication is complete, accurate, up-to-date or fit for any purpose; and (b) Financial Decisions nor its employees are in any way liable to you (including for negligence) in respect of any reliance upon such information or advice. September 2016

Contact: Financial Decisions PO Box 484 Mona Vale NSW 1660, T 02 9997 4647, F 02 9997 7407